The Compound Interest Calculator: The Ultimate Tool for Wealth Building

1. Introduction: The Eighth Wonder of the World

Albert Einstein once reportedly said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

Whether or not Einstein actually uttered these exact words, the sentiment remains universally true. Compound interest is the single most powerful force in personal finance. It is the engine that turns modest, consistent savings into substantial, life-changing wealth over time.

Yet, despite its importance, the vast majority of people underestimate its impact. They see a 7% annual return and think, “That’s just 7% — it doesn’t matter much.”

But when you apply that 7% over 30 years, with regular contributions, the result is often staggering. This is where the Compound Interest Calculator becomes an indispensable professional tool.

A Compound Interest Calculator transforms vague assumptions into concrete projections. It provides clarity, builds confidence, and empowers informed decision-making. Whether you are a financial advisor, a corporate planner, or an individual investor, mastering this tool is non-negotiable.

In this professional guide, we will dissect the mechanics of the calculator, explore advanced features, analyze real-world scenarios, and address common pitfalls. By the end, you will not only understand how to use the calculator—you will understand how to leverage it for strategic financial planning.

2. What Is Compound Interest? (The Core Principle)

Before we dive into the calculator itself, we must establish a clear understanding of compound interest.

2.1 Simple Interest vs. Compound Interest: The Critical Difference

- Simple Interest is calculated only on the original principal amount. If you invest $10,000 at 5% simple interest per year, you earn $500 every year, regardless of how long the money stays invested. The interest does not earn interest.

- Compound Interest is calculated on both the initial principal and the accumulated interest from previous periods. This creates a “snowball effect.” Each period, your interest is added to the principal, and the next interest calculation is based on the larger total.

Professional Example:

- $10,000 invested for 20 years at 7% simple interest → Final value = $24,000.

- $10,000 invested for 20 years at 7% compound interest (compounded annually) → Final value = $38,696.

The difference is $14,696 — and that gap widens exponentially with time.

2.2 The Mathematical Formula Behind Compounding

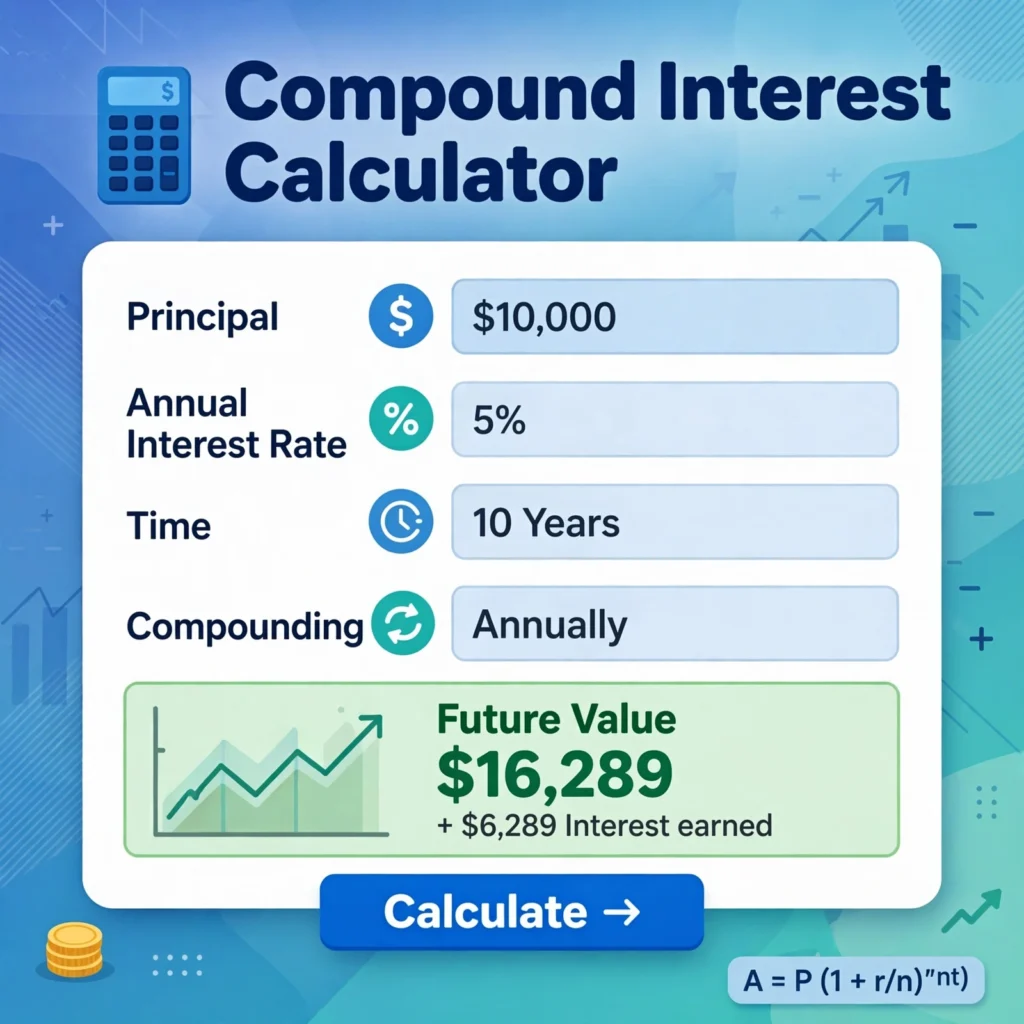

The standard formula for compound interest is:

A = P × (1 + r/n)^(n×t)

Where:

- A = Final amount (including interest)

- P = Initial principal (starting balance)

- r = Annual interest rate (expressed as a decimal, e.g., 7% = 0.07)

- n = Number of times interest is compounded per year

- t = Number of years the money is invested

A professional-grade calculator automates this formula, allowing you to explore multiple variables simultaneously without manual computation.

3. What Is a Compound Interest Calculator?

3.1 The Purpose and Function of the Tool

A Compound Interest Calculator is a digital financial modeling tool that projects the future value of an investment based on:

- Initial capital

- Regular contributions

- Interest rate

- Compounding frequency

- Time horizon

The calculator performs the heavy mathematical lifting, providing an accurate, visual representation of growth over time. It outputs a clear table or graph showing:

- The final balance

- Total contributions made

- Total interest earned

- Year-by-year breakdown of growth

3.2 Who Should Use It?

- Individual Investors: To plan for retirement, education, or major purchases.

- Financial Advisors: To illustrate growth scenarios and demonstrate the value of early investing to clients.

- Corporate Finance Professionals: To model pension fund growth, employee 401(k) projections, or corporate reserves.

- Educators: To teach students the practical application of exponential growth.

4. The Essential Inputs: What Every Calculator Requires

To generate accurate projections, you must input the following five variables:

4.1 Initial Principal (Starting Capital)

This is the lump sum you are starting with today. It could be:

- An inheritance

- A bonus check

- A rollover from a previous retirement account

- Cash you have saved specifically for investment

Professional Tip: Do not include money you need for immediate expenses. This amount should be truly “investable” capital.

4.2 Monthly or Annual Contribution (Regular Deposits)

Most investors contribute regularly—through 401(k) deductions, IRA contributions, or automatic transfers to a brokerage account.

- Monthly Contribution: Best for employees with recurring payroll deductions.

- Annual Contribution: Suitable for those who make lump-sum deposits once a year (e.g., tax refunds or year-end bonuses).

Professional Tip: Consistency is more important than amount. A $200/month contribution consistently over 20 years significantly outperforms irregular, larger contributions made sporadically.

4.3 Annual Interest Rate (The Growth Engine)

This is the expected rate of return on your investment. The appropriate rate depends on your asset allocation:

| Asset Class | Average Annual Return (Historical) |

|---|---|

| S&P 500 (Stocks) | 7% – 8% (inflation-adjusted) |

| Bonds | 3% – 4% |

| Real Estate | 4% – 6% |

| High-Yield Savings | 1% – 2% |

Professional Note: Always use a conservative estimate. A high-risk portfolio might return 12% in a bull market but could lose 30% in a downturn. For planning purposes, 6% – 7% is a realistic, prudent baseline.

4.4 Compounding Frequency (Daily, Monthly, Quarterly, Annually)

This is the number of times per year that interest is calculated and added to the principal.

- Daily: Most common for savings accounts and money market funds.

- Monthly: Common for credit cards, mortgages, and some investment accounts.

- Quarterly: Common for certain bonds and dividend reinvestment plans.

- Annually: Common for certificates of deposit (CDs) and some fixed-rate investments.

Professional Insight: While daily compounding yields slightly more than annual compounding, the difference is marginal over long periods. The real driver of growth is the rate of return and time, not the compounding frequency.

4.5 Time Horizon (Investment Duration in Years)

This is the number of years your money will remain invested and compounding.

- Short-term (1–5 years): Suitable for low-risk, low-return investments.

- Medium-term (5–15 years): Suitable for balanced portfolios.

- Long-term (15–40 years): Suitable for growth-oriented equity portfolios.

Professional Rule: Time is the most critical variable. The longer your horizon, the more dramatic the impact of compounding. Every additional year of growth can significantly alter the final balance.

5. Professional Analysis: How Compounding Frequency Affects Your Returns

5.1 Daily Compounding vs. Annual Compounding: The Math Explained

Consider a $10,000 investment at 7% over 10 years:

| Compounding Frequency | Final Balance |

|---|---|

| Annual | $19,671 |

| Semi-Annual | $19,797 |

| Quarterly | $19,861 |

| Monthly | $19,901 |

| Daily | $19,918 |

Observation: The difference between annual and daily compounding is only $247 over 10 years.

Professional Takeaway: Do not obsess over compounding frequency. Focus on the interest rate, contribution amount, and time horizon. These are the true drivers of wealth accumulation.

5.2 The Rule of 72 (Estimating Doubling Time)

The Rule of 72 is a quick mental shortcut to estimate how long an investment will take to double.

Formula: 72 ÷ Annual Interest Rate = Years to Double

- At 6% → 72 ÷ 6 = 12 years

- At 8% → 72 ÷ 8 = 9 years

- At 10% → 72 ÷ 10 = 7.2 years

Professional Application: This rule helps you quickly communicate growth potential to clients or stakeholders without needing a calculator.

6. Advanced Features of a Professional-Grade Compound Interest Calculator

Basic calculators provide a single output. Advanced calculators offer deeper insights:

6.1 Inflation Adjustment (Real vs. Nominal Returns)

- Nominal Return: The raw percentage return without adjusting for inflation.

- Real Return: The return after accounting for inflation (usually 2% – 3% annually).

Example: If your nominal return is 7% and inflation is 3%, your real return is 4%.

A professional calculator will show both values, allowing you to plan in “today’s dollars” rather than inflated future dollars.

6.2 Tax Considerations (Taxable vs. Tax-Advantaged Accounts)

- Taxable Accounts: Interest is taxed annually, reducing effective returns.

- Tax-Advantaged Accounts (401(k), IRA): Growth is tax-deferred or tax-free.

Advanced calculators allow you to input your marginal tax rate, giving you a more accurate after-tax projection.

6.3 Contribution Escalation (Increasing Deposits Over Time)

As your income grows, your contributions can grow. A robust calculator lets you input an annual escalation rate (e.g., increasing contributions by 3% per year to match inflation or salary growth).

6.4 Withdrawal and Retirement Projections

Some advanced calculators allow you to model partial or full withdrawals during retirement, helping you determine:

- How long your savings will last.

- The sustainable withdrawal rate.

- The impact of early retirement.

7. Real-World Applications: Three Professional Scenarios

Scenario 1: The Early Starter (Age 25, Disciplined Saving)

- Initial Principal: $5,000

- Monthly Contribution: $500

- Annual Interest Rate: 7%

- Compounding: Monthly

- Time Horizon: 40 years (until age 65)

Calculator Result:

- Total Contributions: $245,000

- Final Balance: $1,291,000

- Total Interest Earned: Over $1 million

Professional Insight: This demonstrates the power of starting early. The discipline of $500/month, combined with 40 years of compounding, creates a seven-figure nest egg.

Scenario 2: The Late Bloomer (Age 45, Aggressive Catching Up)

- Initial Principal: $20,000

- Monthly Contribution: $1,200

- Annual Interest Rate: 7%

- Compounding: Monthly

- Time Horizon: 20 years (until age 65)

Calculator Result:

- Total Contributions: $308,000

- Final Balance: $622,000

Professional Insight: The late bloomer contributes more each month but cannot overcome the lost decade of compounding. This illustrates why starting early is the single most valuable financial advantage.

Scenario 3: The Lump-Sum Investor (Inheritance or Bonus Allocation)

- Initial Principal: $100,000

- Monthly Contribution: $0

- Annual Interest Rate: 7%

- Compounding: Monthly

- Time Horizon: 30 years

Calculator Result:

- Total Contributions: $100,000

- Final Balance: $812,000

Professional Insight: A single lump sum, if invested wisely and given sufficient time, can generate enormous wealth without ongoing contributions.

8. Common Professional Pitfalls When Using Compound Interest Calculators

Pitfall 1: Assuming a Constant Rate of Return

Markets do not grow at a constant rate. They experience volatile upswings and downswings. Using a constant 7% projection is useful for planning, but it is not a guarantee.

Mitigation: Run three scenarios:

- Conservative (5%)

- Moderate (7%)

- Optimistic (9%)

This provides a range of possible outcomes.

Pitfall 2: Ignoring the Impact of Fees and Expenses

Investment fees (expense ratios, advisory fees, trading costs) reduce your effective return. A 1% fee might sound small, but over 30 years, it can consume 20% – 30% of your final balance.

Mitigation: Use a calculator that allows you to input expense ratios or management fees.

Pitfall 3: Overlooking Inflation Erosion

A $1 million balance in 30 years may sound impressive. But at 3% annual inflation, its purchasing power in today’s dollars is only about **$412,000**.

Mitigation: Always review the “Real Return” or “Inflation-Adjusted” output.

Pitfall 4: Confusing Nominal and Real Returns

Many investors look at a 10% nominal return and think they are rich. But if inflation is 3% and taxes are 2%, the real after-tax return is only 5%.

Mitigation: Always evaluate your returns net of inflation and taxes.

9. Strategic Application: Using the Calculator for Financial Planning

9.1 Setting Retirement Targets

- Determine your desired annual retirement income.

- Apply the 4% Rule (Total Nest Egg = Annual Income ÷ 0.04).

- Use the calculator to determine the monthly contribution required to hit that target.

9.2 Education Savings (529 Plans)

- Determine the expected cost of college in 18 years.

- Use the calculator to project the required monthly contribution to a 529 plan.

9.3 Debt Management (The Negative Side of Compounding)

Compound interest works against you when you are borrowing. Credit card interest, compounded daily at 24%, can double your debt in just over 3 years.

Professional Advice: Use the calculator in reverse. Input your debt amount, interest rate, and desired payoff timeframe to calculate the monthly payment required.

10. The Psychology of Compounding: Why Patience Is a Competitive Advantage

Compound interest is mathematically powerful, but it requires behavioral discipline.

- The first 10 years of growth are modest and often discouraging.

- The final 10 years of growth are explosive and transformational.

The Curve:

- Year 1–10: Slow, steady accumulation.

- Year 11–20: Acceleration begins.

- Year 21–30: Explosive, exponential growth.

Professional Insight: The greatest enemy of compounding is impatience. Investors who abandon their strategy during the “slow years” miss the exponential payoff. The calculator helps visualize this curve, reinforcing the importance of staying the course.

11. Conclusion: Compound Interest Is Not a Mystery—It Is a Math Problem You Can Solve

The Compound Interest Calculator is not a gimmick. It is a rigorous, data-driven tool that transforms abstract financial concepts into concrete projections.

It reveals the truth about your financial future—whether that truth is comforting or uncomfortable.

- If the calculator shows you are on track, it validates your discipline.

- If it shows you are behind, it empowers you to make strategic adjustments.

Time is your most valuable asset. Contribution consistency is your most reliable strategy. And compound interest is the engine that converts both into lasting wealth.

Your Action Plan:

- Determine your investment goals.

- Gather your financial data (balance, contributions, expected return).

- Use a reliable, professional-grade Compound Interest Calculator.

- Review your projections annually and adjust as needed.

- Stay disciplined, stay invested, and let time do the heavy lifting.

Disclaimer: This article provides professional educational information about compound interest and financial calculators. It does not constitute financial advisory services, investment advice, or a guarantee of future returns. Past performance does not guarantee future results. For personalized financial guidance, consult a licensed financial planner, investment advisor, or tax professional.