The Retirement Calculator: Your 401(k) Crystal Ball for a Stress-Free Future

1. Introduction: The $1 Million Question Nobody Wants to Answer

Close your eyes for a second. Imagine yourself at age 65.

Picture your life. Are you traveling the world? Spending time with grandchildren? Enjoying a quiet morning on a patio with a cup of coffee? Or are you still working a part-time job at a grocery store because you can’t afford to retire?

Here is the terrifying truth: Most Americans have no idea how much money they need to retire. They guess. They hope. They cross their fingers and pray that Social Security will save them.

But here is the good news: you don’t have to guess.

A Retirement Calculator (often called a 401(k) Calculator) is the single most powerful tool for taking control of your financial future. It doesn’t give you a vague “maybe” — it gives you a hard number. It tells you exactly how much you need to save today to enjoy the retirement you dream of tomorrow.

Whether you are 22 years old and just starting your first job, or 50 years old and panicking about being behind, this calculator is your roadmap.

In this guide, we will break down exactly how to use a 401(k) calculator, why compound interest is the “eighth wonder of the world,” and how to fix your savings plan if you are running behind. Let’s get started.

2. Why the “I’ll Start Saving Later” Mentality Is Destroying Your Future

Let me ask you a question: If I offered you $100,000 today, or I offered you $1 million in 40 years, which would you take?

Most people take the $100,000 today. And that is exactly why most people fail at retirement savings.

The human brain is hardwired for instant gratification. We want the new car now. We want the vacation now. We want the nice dinner now.

But the reality is this: Every year you delay saving for retirement costs you thousands of dollars in future growth.

Consider this:

- If you save $5,000 a year starting at age 25, by age 65, you will have approximately **$1.2 million** (assuming a 7% annual return).

- If you wait until age 35 to start saving that same $5,000 a year, by age 65, you will have only **$550,000**.

That is a $650,000 difference — just for waiting 10 years.

This is why a Retirement Calculator is not a luxury. It is a necessity. It forces you to see the math, and the math doesn’t lie.

3. What Is a Retirement Calculator (and What Does It Actually Do)?

At its core, a Retirement Calculator (or 401(k) Calculator) is a financial forecasting tool.

It takes your current financial data and projects it forward into the future. Think of it as a “time machine” for your money.

Here is what it does in plain English:

- It looks at how much money you have saved right now.

- It adds your monthly contributions (your 401(k) deductions).

- It applies an estimated annual growth rate (the interest your investments earn).

- It adjusts for inflation (because $1 today won’t buy the same groceries in 30 years).

- And finally, it tells you: “Based on this, you will have $X by age 65.”

But it doesn’t stop there. A good calculator also tells you:

- Will this amount be enough to cover your living expenses?

- When will you run out of money?

- What do you need to change to reach your goal?

It turns your vague hopes into concrete, actionable data.

4. The Magic of Compound Interest: The #1 Reason You Need a 401(k) Calculator

To understand the calculator, you must understand the engine that powers it: Compound Interest.

Albert Einstein famously called compound interest the “eighth wonder of the world.” Here is why.

4.1 How Compound Interest Works (The Snowball Effect)

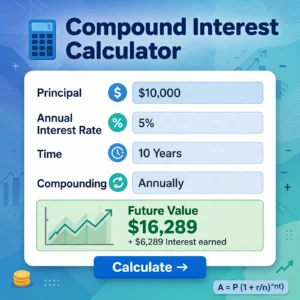

Compound interest is interest earned on interest.

Imagine you invest $10,000 and earn 7% in the first year. You now have $10,700. In the second year, you earn 7% on that new total—$10,700. So your earnings are now $749, not just $700.

This effect snowballs over time. The longer your money sits, the faster it grows.

4.2 The “Time” Factor: Why Starting at 25 vs. 35 Costs You a Fortune

Let’s run a simple comparison using the calculator.

- Option A: Start at age 25. Save $500/month for 40 years. At 7% annual return, you’ll have **$1.2 million**.

- Option B: Start at age 35. Save $500/month for 30 years. At 7% annual return, you’ll have **$590,000**.

The difference is over $600,000 — and it all comes down to the “extra” 10 years of compound growth.

The 401(k) calculator will show you this visualization in a simple graph. And once you see that graph, you will never want to delay saving again.

5. The 5 Essential Inputs Every Retirement Calculator Needs

To get an accurate result, you need to feed the calculator accurate data. Here are the five inputs you must have ready:

5.1 Your Current Age (The Starting Line)

This is simple. Just enter your current age. The calculator needs this to know how many years you have left to grow your money.

5.2 Your Desired Retirement Age (The Finish Line)

This is the age you want to stop working. Most people choose 65 (the traditional retirement age), but many are now aiming for 60, 67, or even 70.

Warning: If you choose a younger retirement age, the calculator will tell you that you need to save significantly more money each month because you have fewer years to grow your nest egg.

5.3 Your Current 401(k) Balance (Your Head Start)

This is the total amount you have already saved across all your retirement accounts (401(k), IRA, Roth IRA, etc.). Even if it’s only $500, it matters. The calculator will compound this amount from today forward.

5.4 Your Monthly Contribution (The Fuel)

This is the amount you are currently putting into your 401(k) or IRA each month.

Important: This does not include your employer’s match. That comes later. For now, enter only what you contribute out of your own paycheck.

5.5 Your Expected Annual Rate of Return (The Growth Engine)

This is the trickiest input, and it’s where many people make mistakes.

- Optimistic guess: 10% (This is what many inexperienced investors use. It’s unrealistic over the long term.)

- Realistic guess: 7% to 8% (This is the historical average return of the S&P 500 stock market over the last 70 years.)

- Conservative guess: 5% (If you invest heavily in bonds or safer assets.)

Our Recommendation: Use 7% as your baseline. Then, run the calculator again at 5% to see the “worst-case” scenario. The calculator will show you how much your final balance changes based on this number.

6. Beyond the Basics: Advanced Features of a Smart 401(k) Calculator

Basic calculators give you a rough number. Smart calculators give you a detailed retirement blueprint. Here are the advanced features you should look for:

6.1 The Employer Match (Free Money You Can’t Ignore)

Many employers offer a 401(k) match. For example, they may say, “We will match 50% of your contributions up to 6% of your salary.”

This means if you contribute 6% of your paycheck, your employer adds an extra 3%. That is free money.

- Example: If you earn $60,000 and contribute 6% ($3,600), your employer adds $1,800. That’s a 50% immediate return on your investment.

A good calculator will ask for your employer’s match percentage and add it to your total contribution. If your calculator doesn’t have this feature, you are missing out on a huge part of your retirement picture.

6.2 Inflation Adjustments (Why $1 Million Won’t Be Enough in 30 Years)

Here is a terrifying fact: The cost of living doubles roughly every 20 years.

If you retire with $1 million today, that might seem like a fortune. But in 30 years, due to inflation, that $1 million will only have the buying power of about $400,000 in today’s dollars.

A smart calculator automatically adjusts your final balance for inflation. It shows you your “real” retirement income in today’s dollars, so you don’t get a false sense of security.

6.3 Social Security Estimator (The Government’s Safety Net)

Many people think, “I don’t need to save much because Social Security will cover me.”

That is a dangerous assumption. Social Security currently replaces only about 40% of your pre-retirement income for the average earner. Most financial experts recommend having enough savings to cover 70% to 80% of your pre-retirement income.

A good calculator will estimate your Social Security benefits and subtract them from your total required retirement income, showing you exactly how much you need to cover out of your own savings.

7. How to Use the Calculator to Set Realistic Retirement Goals

Okay, you’ve plugged in your numbers. The calculator gives you a final balance. Now what?

Here is how to interpret that number and turn it into a plan.

Step 1: The 4% Rule (How Much Money You Need to Retire)

Financial experts often use the 4% Rule to estimate how much money you need to retire.

The rule says: “You can safely withdraw 4% of your retirement savings in your first year of retirement, and then adjust that amount for inflation each year, without running out of money for 30 years.”

How does this translate to your goal? Here is the simple math:

- If you want $40,000 per year in retirement income, you need a nest egg of **$1,000,000** ($40,000 ÷ 0.04).

- If you want $60,000 per year, you need **$1,500,000**.

- If you want $80,000 per year, you need **$2,000,000**.

The 401(k) calculator will tell you if your projected balance meets this 4% withdrawal target.

Step 2: The “Retirement Income Gap” Test

Take your estimated annual expenses in retirement (housing, food, healthcare, travel) and subtract your projected Social Security income. The difference is the “income gap” you need to cover from your own savings.

- Example: You estimate you’ll need $60,000/year. Social Security will pay you $24,000/year. Your gap is $36,000/year.

Using the 4% rule, you need a nest egg of $36,000 ÷ 0.04 = **$900,000**.

The calculator will tell you if you are on track to hit that $900,000 target. If not, it’s time to adjust your contributions.

Step 3: The “Stress Test” (What Happens If the Market Crashes?)

Markets crash. It happens every 7 to 10 years.

A good calculator allows you to run a “stress test.” You can input a scenario where the market drops by 20% or 30% in the first 5 years of your retirement.

If the calculator shows that you would run out of money in that scenario, you might need to:

- Keep a larger cash emergency fund.

- Reduce your withdrawal rate to 3.5%.

- Work a few more years to let the market recover.

8. The “Good News” vs. “Bad News” Scenarios (What Your Calculator Will Tell You)

When you run the calculator, you will get one of three results:

Scenario A: You’re on Track (The Green Light)

The calculator shows that you will have exactly what you need, or even more.

Action: Celebrate! But don’t get complacent. Run the calculator once a year to ensure you stay on track. Consider increasing your contributions when you get a raise.

Scenario B: You’re Behind (The Yellow Flag)

The calculator shows a shortfall. You are projected to have only 60% to 80% of what you need.

Action: This is fixable. Don’t panic. Use the “Fix Your Plan” section below to make small adjustments.

Scenario C: You’re in Trouble (The Red Alert)

The calculator shows you have less than 50% of what you need, or you are projected to run out of money by age 80.

Action: This is serious, but not hopeless. You will need to make significant changes, such as increasing your savings rate dramatically, delaying retirement, or downsizing your retirement lifestyle. The calculator can help you see exactly how much you need to change.

9. How to Fix a “Behind” Scenario Without Panicking

If the calculator shows a shortfall, here are three things you can do to get back on track.

9.1 Increase Your Contribution Rate (Even 1% Helps)

Most 401(k) plans allow you to change your contribution percentage at any time.

- Action: Increase your contribution by just 1% or 2%.

- The Impact: If you earn $60,000 and increase your contribution by 2%, you are adding $100/month. Over 30 years at 7% return, that extra $100/month turns into **$113,000** at retirement.

9.2 Delay Your Retirement Age (Work 2 More Years)

This is the single most effective way to fix a shortfall.

Working 2 more years means:

- You delay withdrawing from your savings.

- You add 2 more years of contributions.

- You give your investments 2 more years of compound growth.

- Your Social Security benefits increase (because you delayed claiming them).

Just two extra years of work can increase your retirement income by $20,000 to $40,000 per year.

9.3 Reduce Your Expected Retirement Spending

The calculator asks you how much you expect to spend in retirement. If that number is too high, you can lower it.

- Action: Plan to travel less frequently. Downsizing your home. Moving to a lower-cost city.

- The Impact: Reducing your annual retirement spending by $10,000 means you need $250,000 less in your nest egg ($10,000 ÷ 0.04).

10. Common Retirement Calculator Mistakes That Skew Your Results

Avoid these three traps to ensure your calculator gives you accurate results.

Mistake 1: Using an Unrealistic Rate of Return (10% vs. 7%)

Many people see the stock market grow by 20% in one year and think, “I can average 10% annually.”

The Reality: The stock market historically averages about 7% to 8% after inflation. And there are years of losses mixed in. Always use a conservative estimate (7%) and run a worst-case scenario (5%).

Mistake 2: Ignoring Inflation (The Silent Thief)

If your calculator does not automatically adjust for inflation, your final number will be wildly inaccurate.

Example: You project a $1 million balance at age 65. But if inflation averages 3% over 30 years, that $1 million will only buy what $400,000 buys today. Always use a calculator that converts your final balance into “today’s dollars.”

Mistake 3: Forgetting About Taxes (Roth vs. Traditional 401(k))

- Traditional 401(k): Contributions are pre-tax (you don’t pay tax today), but withdrawals in retirement are taxed as ordinary income.

- Roth 401(k): Contributions are post-tax (you pay tax today), but withdrawals in retirement are tax-free.

If you have a Traditional 401(k), your actual spending power is lower because you will owe taxes on every dollar you withdraw. A good calculator accounts for this by asking what tax bracket you expect to be in during retirement.

11. Seasonal Spikes: When to Max Out Your 401(k) Contributions

Most people set their 401(k) contribution and forget about it. But there are specific times of year when you can accelerate your savings.

11.1 The “Year-End” Rush (December Catch-Up)

The IRS has annual contribution limits. For 2026, you can contribute up to $23,000 to a 401(k) (plus an extra $7,500 if you’re over 50).

If you haven’t maxed out your contributions by December, you can increase your deduction in your final paychecks to hit the limit. Use the calculator to see how hitting the max affects your retirement balance.

11.2 The “Bonus” Windfall (Using Extra Cash for Retirement)

If you receive a work bonus or a tax refund, don’t spend it on a new TV. Use the calculator to see what happens if you put that extra cash directly into your 401(k).

- Example: A $5,000 bonus invested at age 35 at 7% return will grow to **$38,000** by age 65. That is a massive return on “extra” money.

12. Conclusion: The Best Time to Start Was Yesterday. The Second Best Time Is Now.

Retirement planning is not about perfection. It is not about hitting an exact number and then “checking out.” It is about progress.

The Retirement Calculator (401(k) Calculator) is your personal financial compass. It shows you where you are, where you need to go, and exactly how to get there.

Whether you are 25 years old and saving $100/month, or 55 years old and playing catch-up, the calculator gives you a plan. It replaces fear with facts. It replaces anxiety with action.

Here is your call to action:

- Log into your 401(k) or IRA account.

- Check your current balance.

- Find your current monthly contribution.

- Open a reliable Retirement Calculator.

- Plug in your numbers and see your future.

The answer might surprise you. It might scare you. But it will never lie to you. And once you see the truth, you can finally take control.

Your future self is counting on you. Start now. Don’t wait another day.