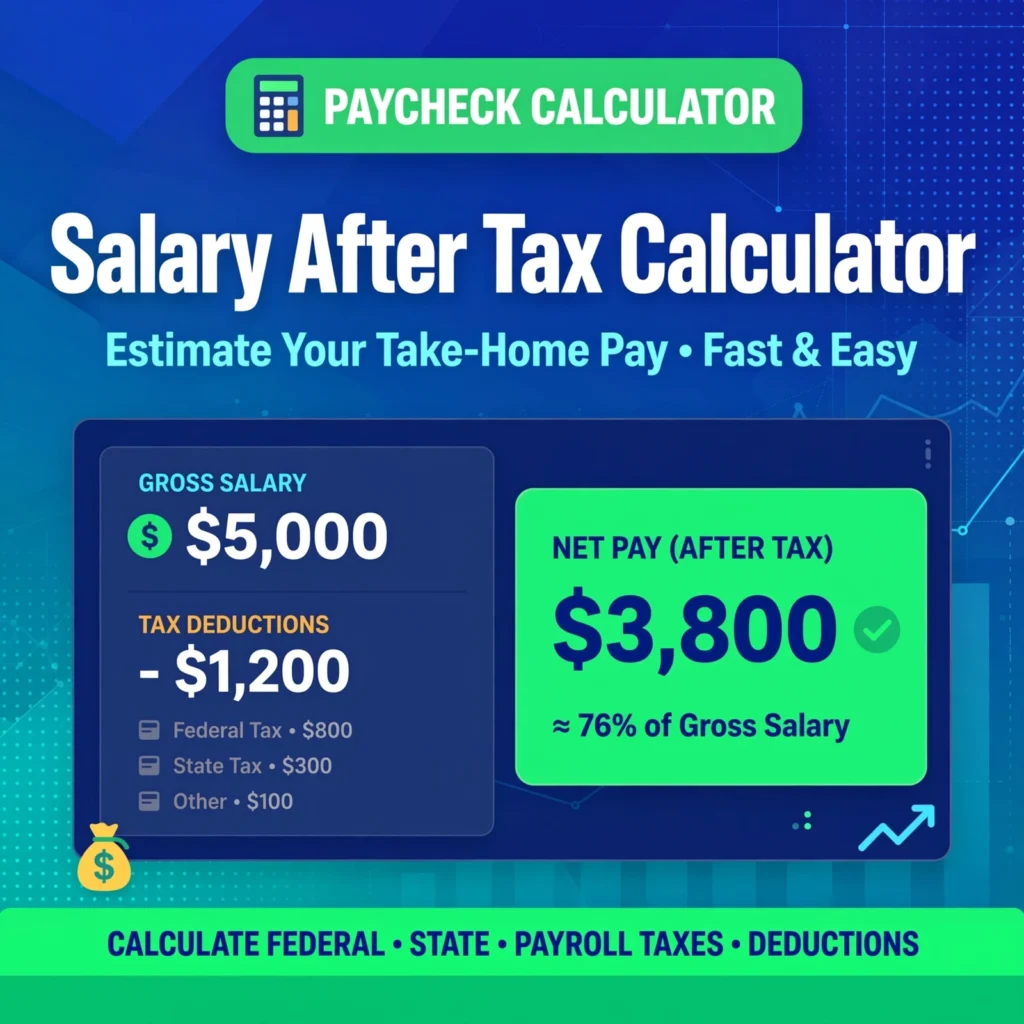

Net Pay vs. Gross Pay: The Ultimate Paycheck Calculator Guide for Every Worker

1. Introduction: The $10,000 Question Nobody Asks

You land a new job. The offer letter says **$80,000 per year**. You do the math in your head: $80,000 ÷ 12 months = $6,666 per month. You imagine upgrading your apartment, saving for a down payment, and finally taking that trip to Europe.

Then, your first paycheck arrives.

It’s $4,800.

Where did nearly $2,000 go? Did the company make a mistake? Did you sign up for too many benefits? Or is this just… normal?

The Paycheck Calculator (also called a Salary After Tax Calculator) is the only tool that answers this question honestly. It takes your shiny “gross salary” and strips away all the hidden taxes, deductions, and fees to reveal your net pay — the number that actually hits your bank account.

But here is the secret most people don’t know: You have more control over your net pay than you think. By understanding how the calculator works, you can adjust your withholdings, time your bonuses, and even choose where you live to keep more money in your pocket.

In this guide, we will break down every single deduction, teach you how to use advanced calculator features, and reveal the seasonal spikes that can shrink your paycheck without warning. Let’s get started.

2. Gross vs. Net: The Two Numbers That Define Your Life

Before you touch the calculator, you must understand the difference between these two numbers. They are not the same, and they never will be.

2.1 Gross Pay (The “Headline” Number)

Gross pay is your total earnings before any deductions. This includes:

- Your base salary or hourly wages

- Overtime pay

- Bonuses and commissions

- Tips and gratuities (if you are in a tipped profession)

This is the number on your job offer. This is the number on your employment contract. This is the number you tell your parents when they ask how much you make.

But gross pay is a fantasy. You will never see this full amount in your bank account.

2.2 Net Pay (The “Reality” Number)

Net pay is what remains after all taxes, insurance premiums, retirement contributions, and other deductions are taken out.

This is your “take-home pay.” This is what you use to pay rent, buy groceries, and save for your future. This is the number that matters for your daily life.

2.3 Why the Gap Matters for Your Budget

Here is a hard truth: If you budget based on gross pay, you will fail.

People who budget based on gross pay often overestimate their spending power by 25% to 35%. They sign a lease for an apartment they can’t afford. They buy a car they can’t finance. They end up in credit card debt because they never accounted for the “gap.”

Your Paycheck Calculator closes that gap. It forces you to look at reality, not fantasy.

3. The Seven Deductions That Shrink Your Paycheck

To understand your net pay, you must know exactly what is being taken out. Here are the seven deductions that appear on every pay stub:

3.1 Federal Income Tax (Progressive Brackets Explained Simply)

The IRS uses a progressive tax system. This does NOT mean all your income is taxed at the same rate. It means:

- The first $11,600 of your income is taxed at 10%

- The next $35,500 is taxed at 12%

- The next $53,300 is taxed at 22%

- And so on…

Example: If you earn $80,000, you do NOT pay 22% on all $80,000. You pay 10% on the first chunk, 12% on the next chunk, and 22% only on the portion above $47,150. Your effective tax rate is much lower than your marginal tax rate. The calculator shows you both numbers.

3.2 State Income Tax (The 9 States That Keep 100% of Your Money)

This is where geography changes your financial life. There are 9 states with NO state income tax:

- Texas, Florida, Nevada, Washington, Wyoming, Alaska, South Dakota, Tennessee, and New Hampshire.

If you live in California or New York, your state tax can be as high as 10% to 13.3%. The calculator will show you the exact dollar amount.

3.3 FICA (Social Security & Medicare – The Invisible Tax)

This is the 7.65% payroll tax that funds Social Security and Medicare.

- Social Security: 6.2% (capped at $168,600 in 2026)

- Medicare: 1.45% (no cap, plus an extra 0.9% if you earn over $200,000)

Your employer matches this amount, so the total contribution is actually 15.3%. But you only see the 7.65% on your pay stub.

3.4 Federal Unemployment Tax (FUTA) – Not Your Problem, But Worth Knowing

Employers pay FUTA, not employees. You don’t see this on your pay stub. However, it’s worth knowing because it explains why employers are sometimes hesitant to hire — they pay unemployment insurance for you.

3.5 Pre-Tax 401(k) Contributions (The “Pay Yourself First” Strategy)

This is the most powerful deduction because it saves you money on taxes. When you contribute to a traditional 401(k), that money comes out of your gross pay before taxes are calculated.

- Example: If you earn $80,000 and contribute $5,000 to your 401(k), the IRS taxes you on only $75,000. This lowers your federal and state tax bill immediately.

3.6 Health Insurance Premiums (The Employer-Provided Benefit)

Most employers offer health insurance, and the premiums are deducted pre-tax. This reduces your taxable income further. The calculator asks for your monthly premium to get an accurate net pay number.

3.7 Post-Tax Deductions (Garnishments, Union Dues, Child Support)

These are taken out after all taxes are calculated.

- Child Support: Court-ordered payments

- Garnishments: Credit card or student loan wage garnishments

- Union Dues: If you are in a unionized profession

These are non-negotiable. The calculator subtracts them from your final net pay.

4. How to Use a Paycheck Calculator Correctly (Step-by-Step)

Most people skip steps and get wrong results. Here is the proper way to use a Paycheck Calculator:

Step 1: Input Your Gross Annual Income Accurately

If you are hourly, multiply your hourly rate by 2,080 hours (40 hours × 52 weeks). If you work overtime, calculate your average weekly hours and multiply by 52.

Step 2: Select Your Filing Status (Single, Married, Head of Household)

This changes your standard deduction and tax brackets.

- Single: Standard deduction is $14,600 (2026)

- Married Filing Jointly: Standard deduction is $29,200

- Head of Household: Standard deduction is $21,900 (for single parents supporting dependents)

Step 3: Enter Your Pay Frequency (Weekly, Bi-Weekly, Semi-Monthly, Monthly)

- Bi-weekly: 26 paychecks per year

- Semi-monthly: 24 paychecks per year (1st and 15th)

- Monthly: 12 paychecks per year

The calculator will adjust your per-check amount accordingly.

Step 4: Add Your Pre-Tax Deductions (The 401(k) and Insurance Boxes)

Enter your annual 401(k) contribution and your monthly health insurance premium. This will reduce your taxable income and increase your net pay.

Step 5: Adjust Your Withholding Allowances (The W-4 Trick)

The W-4 form tells your employer how much tax to withhold. If you claim fewer allowances, more tax is withheld (bigger refund, smaller checks). If you claim more allowances, less tax is withheld (smaller refund, bigger checks).

The Goal: Aim for a refund as close to $0 as possible. That means you are not giving the government an interest-free loan of your own money.

5. Beyond the Basic Calculator: Advanced Features You Need

Basic calculators give you a number. Advanced calculators give you strategy.

5.1 The “Bonus” Calculator (What a $5,000 Bonus Actually Nets You)

Bonuses are taxed at a flat supplemental rate of 22% federally (plus state tax). If your bonus is $5,000, expect to receive roughly $3,500 to $3,800 after taxes. The calculator shows you this instantly.

5.2 The “Side Hustle” Estimator (1099 vs. W-2 Tax Differences)

If you are a freelancer or independent contractor (1099), you pay both the employee and employer portions of FICA. That means 15.3% instead of 7.65%. The advanced calculator can toggle between W-2 and 1099 to show you the difference.

5.3 The “State-to-State” Comparison Tool

This is the most powerful feature. Enter $100,000 gross in California and Texas side-by-side.

- California Net Pay: ~$65,000

- Texas Net Pay: ~$72,000

That is a $7,000 difference per year — just because of geography.

6. Seasonal Spikes: When Your Paycheck Changes Without Warning

Your paycheck is not constant. Here are three seasonal spikes that affect your net pay:

6.1 The “January Slump” (Why Your January Check Is Smaller)

In January, you start a new tax year. If your employer over-withheld taxes in December (to meet year-end requirements), your January check might be smaller as they adjust to the new tax rates and brackets.

6.2 The “Bonus Tax Bite” (Why Bonuses Are Taxed at Higher Rates)

Bonuses are taxed at a flat 22% federal rate, regardless of your income bracket. This means a $10,000 bonus is taxed at 22% federally, plus state tax, plus FICA. You will receive only about $6,500 to $7,000.

Strategy: Use the calculator to see if a bonus is worth more than a salary increase. Sometimes, a $5,000 salary raise (taxed at your marginal rate) nets you more than a $5,000 bonus (taxed at 22%).

6.3 The “Year-End” Adjustment (How Tax Brackets Shift Annually)

Tax brackets are adjusted for inflation every year. If the standard deduction increases, your tax liability decreases. The calculator updates these numbers annually, so always use the current year’s calculator.

7. Five Common Paycheck Myths Debunked

Let’s clear up the confusion once and for all.

Myth 1: “My employer takes 30% of my income”

False. Your effective tax rate is usually between 12% and 20% for most middle-income earners. The marginal rate (22%) only applies to your highest dollars, not your entire income.

Myth 2: “I can’t change my tax withholding”

False. You can submit a new W-4 to your HR department at any time. If you are getting too much back in refunds, reduce your allowances to get more money now.

Myth 3: “A raise always means more take-home pay”

False. If your raise pushes you into a higher tax bracket, only the income above that bracket is taxed at the higher rate. You always take home more with a raise — just not as much as you expect.

Myth 4: “Bonuses are taxed at a flat 40%”

False. Federal bonus tax is 22%, plus your state tax rate. The total is usually around 30% to 35%, not 40%.

Myth 5: “I don’t need to check my pay stub”

False. Errors happen. I have seen people overpay hundreds of dollars in taxes because their employer misclassified their filing status. Always check your pay stub against your calculator.

8. The “What If” Strategy: Using the Calculator to Negotiate Smarter

Here is how to use the calculator in real-world job negotiations:

8.1 Asking for a Signing Bonus Instead of a Salary Raise

Run the calculator. A $5,000 salary increase nets you about $3,500 more per year (after taxes). A $5,000 signing bonus nets you about $3,500 one time. If you need the cash upfront for moving or relocation, a bonus is better.

8.2 Choosing Between a 401(k) Match and a Higher Base Salary

Your employer offers a 4% 401(k) match. The calculator shows that a 4% match on an $80,000 salary is $3,200 of free money — tax-deferred. Would you rather have $3,200 in free retirement savings or $3,200 in taxable salary? The calculator helps you compare.

8.3 Deciding Between a Remote Job in a High-Tax vs. Low-Tax State

Use the state comparison feature. A $90,000 remote job in California nets you $58,000. The same $90,000 job in Texas nets you $65,000. That is a $7,000 difference. If the California job offers higher growth potential, you might still take it — but at least you know the true cost.

9. Conclusion: Your Paycheck Is Your Power — Calculate It Wisely

The Paycheck Calculator (Salary After Tax Calculator) is not a toy. It is a financial truth-teller.

It exposes the gap between what you think you earn and what you actually earn. It helps you decide between job offers, choose where to live, and plan your budget with precision.

And most importantly, it puts you in control. You can adjust your W-4, increase your 401(k) contributions, and time your bonuses to maximize your net pay.

Your salary is not the number on your contract. Your salary is the number that hits your bank account.

Open a reliable Paycheck Calculator today. Input your numbers honestly. Look at your net pay — and then build your life around that number, not the fantasy.

Your budget will thank you. Your future self will thank you. And you will finally understand why that $80,000 job only pays you $4,800 a month.

Now you know why. Now you know how to fix it.