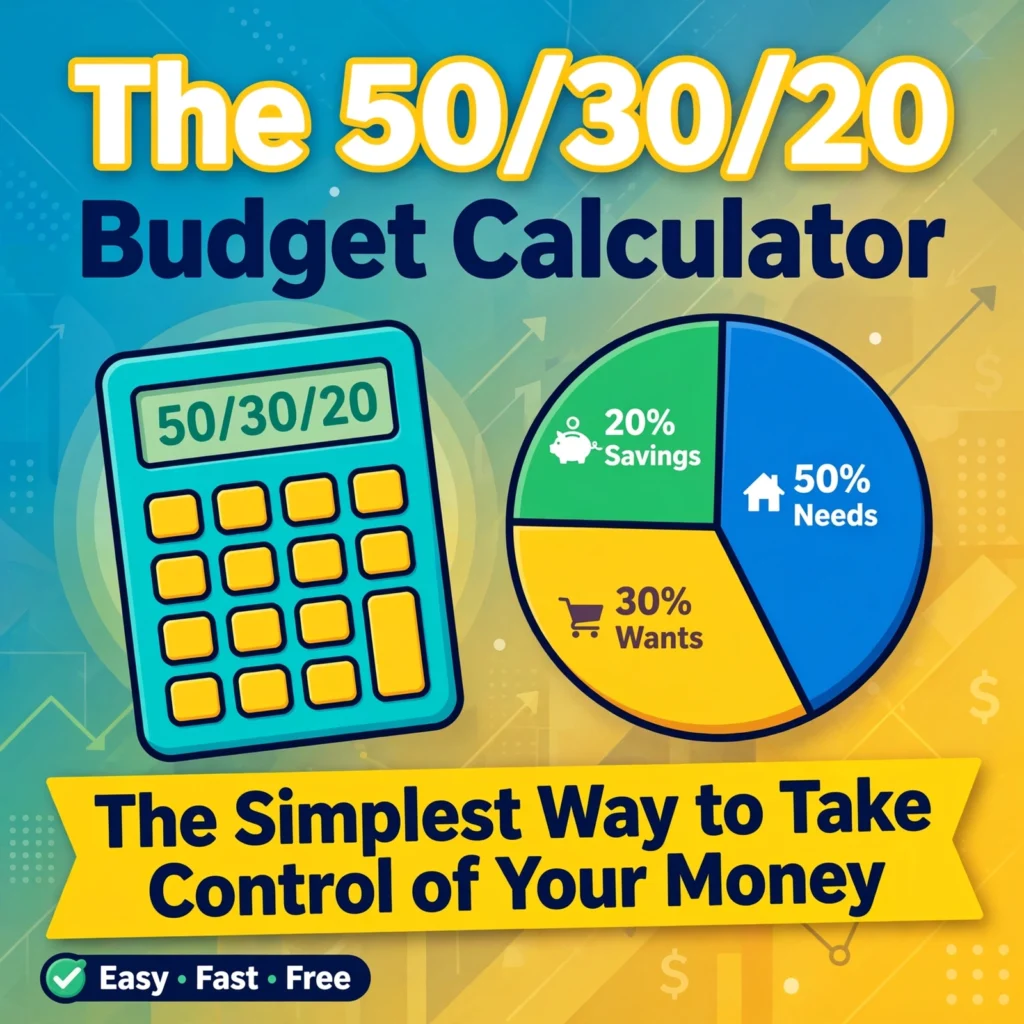

The 50/30/20 Budget Calculator: The Simplest Way to Take Control of Your Money

1. Introduction: Why Most Budgets Fail (And How This One Is Different)

Let’s be honest. When you hear the word “budget,” what comes to mind?

For most people, it’s a feeling of dread. It means spreadsheets. It means tracking every single penny. It means cutting out all the fun in your life. It means living like a monk for 30 days just to save $50.

That is exactly why 90% of traditional budgets fail within the first three months. They are too strict, too complicated, and too boring.

But what if I told you there is a budgeting method that takes less than 5 minutes to set up, allows you to spend money on things you love, and still helps you save for the future?

Enter the 50/30/20 Rule.

This rule is the “gateway drug” to personal finance. It is perfect for beginners (TOFU traffic) who are overwhelmed by complex financial jargon. It doesn’t require you to track every coffee you buy. It gives you a simple, easy-to-remember framework.

And the best part? You don’t need to do the math yourself. A 50/30/20 Budget Calculator does it all for you.

2. What is the 50/30/20 Rule? (The Golden Ratio of Personal Finance)

First popularized by Senator Elizabeth Warren in her book All Your Worth, the 50/30/20 rule is a simple, percentage-based approach to handling your monthly income.

Instead of looking at line items like “groceries” or “gas,” you group your expenses into three broad buckets.

Here is the simple breakdown:

2.1 The 50%: Needs (Your Roof, Your Food, Your Ride)

This is the “survival” bucket. These are the bills you must pay to function in society. If you don’t pay them, you lose your home, your car, or your health.

- What goes here? Rent or mortgage payments, utility bills (electricity, water, gas), car payments, minimum credit card payments, groceries, and basic health insurance.

2.2 The 30%: Wants (Your Netflix, Your Coffee, Your Fun)

This is the “lifestyle” bucket. These are the things that make life enjoyable but are not strictly necessary for survival.

- What goes here? Dining out, takeout food, streaming subscriptions (Netflix, Disney+, Hulu), gym memberships, concert tickets, vacations, shopping for new clothes, and your daily Starbucks run.

Important Note: This bucket is not “bad.” You are allowed to have wants! In fact, this bucket is what keeps you from feeling deprived.

2.3 The 20%: Savings & Debt (Your Future Self’s Best Friend)

This is the “wealth-building” bucket. This money goes toward your future and paying off the past.

- What goes here? Contributions to your 401(k) or IRA, emergency savings, extra payments on your credit card debt (beyond the minimum), student loan payments, and saving up for a down payment on a house.

3. What is a 50/30/20 Budget Calculator? (And Why You Need One)

So, let’s say you bring home $4,000 a month. According to the rule:

- $2,000 goes to Needs (50%)

- $1,200 goes to Wants (30%)

- $800 goes to Savings (20%)

Simple enough, right? But here is the problem: Life is messy. When you get your monthly bank statement, you have 50 different charges. How do you quickly figure out if you are actually hitting those 50/30/20 targets?

A 50/30/20 Budget Calculator is an automated tool that does this categorization for you. You simply plug in:

- Your total monthly take-home pay.

- Your essential bills (rent, utilities, groceries).

- Your discretionary spending.

- Your savings contributions.

The calculator will instantly tell you: “You are spending 55% on Needs (too much), 25% on Wants (good), and 20% on Savings (perfect!).”

It gives you immediate feedback, so you don’t have to dig through spreadsheets trying to figure out if you are on track.

4. How to Use a 50/30/20 Budget Calculator (Step-by-Step)

Using the calculator is easier than ordering a pizza. Here is exactly how to do it:

Step 1: Calculate Your “Net Take-Home Pay”

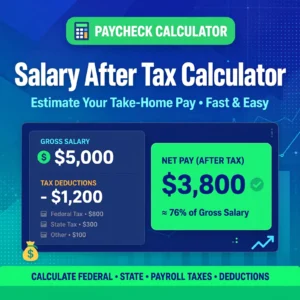

If you haven’t read our guide on the Paycheck Calculator, here is the golden rule: Never budget using your gross salary.

Look at your bank deposit on payday. That number (after taxes, insurance, and 401k) is your true income. If you get paid bi-weekly, multiply your check by 26 and divide by 12 to get your monthly average.

Example: If you get $2,000 every two weeks, your monthly net income is roughly $4,333.

Step 2: Input Your Numbers into the Calculator

Open your preferred 50/30/20 calculator and plug in:

- Total Monthly Take-Home Pay: $4,333

- Total Monthly Needs: (Rent $1,200 + Car $400 + Groceries $400 = $2,000)

- Total Monthly Wants: (Dining out $300 + Netflix $20 + Gym $80 = $400)

- Total Monthly Savings: (401k $300 + Emergency fund $200 = $500)

Step 3: The “Breakdown” Result

The calculator will generate a simple pie chart showing you the percentage breakdown.

- Needs: $2,000 / $4,333 = 46% (You are under the 50% limit! Good job.)

- Wants: $400 / $4,333 = 9% (You are way under 30%—you have room to loosen up!)

- Savings: $500 / $4,333 = 11% (You are only saving 11%—you need to increase this to hit 20%).

Within 30 seconds, you know exactly where you need to adjust your spending.

5. The “Gray Area” Problem: What Counts as a “Need” vs. a “Want”?

This is the #1 question people ask when using the rule. The lines get blurry. Here is how to handle the gray areas:

5.1 The Grocery Store Dilemma

- Need: Basic ingredients (rice, eggs, bread, chicken, vegetables) that you cook at home.

- Want: The gourmet $12 cheese, the fancy pre-cut fruit, and that bag of chips you grabbed at the checkout.

Pro Tip: The calculator wants your actual grocery bill. Don’t overthink it. If you buy it to survive, it’s a Need. If you buy it because it looks tasty, it’s a Want.

5.2 The “Subscription Trap”

Do you have 6 different streaming services? The first one (Netflix) might be a Want. But if you are paying for a gym membership and you never go, that is a wasted want. Cut it out.

5.3 Internet and Phone Bills

In 2026, having internet access is almost essential for work and school. However, the $100/month ultra-fast fiber optic plan might be a Want, while the $50/month basic plan is the Need. If you can downgrade your plan and still survive, you just freed up $50 for your Savings bucket.

6. Why This Method is a Game-Changer for Beginners (TOFU Appeal)

If you have never budgeted before, the 50/30/20 rule is the absolute best place to start. Here is why it converts beginners so well:

6.1 It Overwhelms You Less

Traditional budgets require you to track every penny. That is exhausting. The 50/30/20 rule only asks you to track three numbers. It is simple enough to stick with.

6.2 It Gives You “Permission” to Have Fun

Many people think “budget” means “boring.” This rule specifically gives you a 30% allowance to spend on fun. You don’t have to feel guilty about your Starbucks run—as long as it fits inside your 30% bucket.

6.3 It Automates Your Savings

When you first get your paycheck, the most important thing you can do is move your 20% savings into a separate account immediately. If you don’t see it, you won’t spend it. The calculator helps you visualize this “pay yourself first” mentality.

7. Seasonal Spikes: How to Adjust Your 50/30/20 Budget for the Holidays and Summer

The 50/30/20 rule is a monthly average, but life isn’t perfectly average every month. Here is how to handle seasonal changes:

7.1 The Holiday Slump (November–December)

Your “Wants” bucket will spike during the holidays because of gifts, travel, and parties.

- Strategy: For two months, temporarily reduce your “Savings” bucket from 20% to 10%. Put that extra 10% into your “Wants” bucket. This keeps your budget balanced without dipping into credit cards.

7.2 The Summer Spending Surge (June–August)

Summer is the season of vacations, outdoor dining, and kids’ activities.

- Strategy: If you know you are going on vacation in July, reduce your Needs budget in May and June (cook more at home, carpool to work) so you have extra cash in the Wants bucket for your trip.

A good Budget Calculator will let you adjust these percentages monthly so you can see exactly how it affects your bottom line.

8. The “Zero-Based” vs. “50/30/20” Debate (Which is Right for You?)

You might hear financial gurus talk about “Zero-Based Budgeting” (where every dollar is assigned a specific job). So, which one should you use?

- Zero-Based Budgeting: Best for people with high debt, irregular income, or specific financial goals. It is incredibly detailed but time-consuming.

- 50/30/20 Budgeting: Best for beginners, salaried employees, and people who want a “set it and forget it” approach.

Our Advice: Start with the 50/30/20 rule. If you find that you are not making progress on your debt, then you can graduate to a zero-based budget. But for 80% of people, the 50/30/20 rule is enough to get them out of debt and into savings.

9. Common Mistakes People Make with the 50/30/20 Rule

Avoid these three traps to ensure your calculator gives you accurate results:

Mistake 1: Using Gross Income Instead of Net Income

This is the biggest mistake. If you earn $5,000 gross but take home $3,800, you must use $3,800 in the calculator. Otherwise, you will think you have more money than you actually do.

Mistake 2: Putting “Needs” Before “Savings”

Many people look at their paycheck and pay their rent, then their car, then their groceries—and then they see if they have any money left for savings. Do not do this.

Treat your savings like a fixed expense. If you don’t allocate 20% first, you will never save it. Use the calculator to determine how much you must save before you start buying wants.

Mistake 3: Giving Up When You Go Over Budget

You will have a bad month. You will go out to eat too much. You will buy the expensive shoes. That is okay. The 50/30/20 rule is not about perfection; it’s about awareness.

If you go over 30% on Wants this month, just adjust your spending next month. The calculator gives you the data, but you give yourself the grace.

10. Conclusion: Start Your Financial Journey Today

The 50/30/20 rule is not just a math formula—it is a lifestyle shift.

It says: “Yes, you need to survive. Yes, you deserve to have fun. And yes, you must save for your future.” It validates all three parts of your life, and it gives you a simple road map to follow.

You don’t need a finance degree. You don’t need to be a math wizard. All you need is your monthly take-home pay and a reliable 50/30/20 Budget Calculator.

Are you ready to stop stressing about money and start living your life?

Grab your pay stub, open the calculator, and plug in your numbers. You might be surprised at how much control you actually have over your money.

Take the first step today. Your future self will thank you.

Disclaimer: This article provides general educational information about budgeting and personal finance. It does not constitute professional financial advice. The 50/30/20 rule is a guideline, not a strict rule, and may need to be adjusted based on your personal debt levels, income, and cost of living. For advice specific to your financial situation, please consult a certified financial planner.